LME Averaging

To those unfamiliar with the unique structure of the LME, executing an average hedge can be confusing at best, and intimidating at worst. But averages are nothing to be concerned with, and given that a large proportion of physical contracts utilize averaging to generate their prices, it is a subject you should become acquainted with.

How Averages Are Constructed

There are many different ways that an average can be formed. From as short as a two-day period up to a full month. There are also different settlement prices within each day that can be used to create averages, however the most common method is utilizing the official cash settlement price each day (CSP). The CSP is discovered in the open outcry session of ring 2 for each metal. It is the last offered price prior to the bell in that 2nd ring for each metal. The second most common is using the closing price each day - the market on close (MOS) or kerb price as it's known.

For example, if you have a physical contract that is pricing over the full official cash average of a month, say September, then the price will be the average of every single CSP during the month of September. Looking at September 2025, there are 22 pricing days in the month, so there will be 22 different CSP prices for each metal, with the physical contract receiving the average of these prices.

Where Prompt Dates Add Confusion

All sounds relatively simple so far right? Where the confusion can come in is in the prompt date structure of the LME. Unlike other exchanges, the LME has multiple prompt dates per month. In fact, within the cash (2 business days' time) to 3-month window, every business day is an LME prompt date (barring US bank holidays).

When you buy or sell futures basis a CSP, the natural prompt date for that futures trade would be 2 business days following the date of execution. For example, the prompt date for the CSP on Monday the 1st of September 2025 would be Wednesday the 3rd of September 2025. This pattern continues throughout the month - 2nd Sep CSP has a prompt date of 4th Sep, 3rd Sep CSP has a prompt date of 5th Sep, and so on.

However, the LME is a physically settled exchange, so if you were to leave your futures position open for each CSP, 2 days later it would become a physical obligation. If you were hedging a physical sale and buying futures over the average, you would be obligated to buy warrants from an LME warehouse. If you were hedging a physical purchase and selling futures, you would be obligated to deliver warrants into an LME warehouse.

To avoid this, the natural prompt date for a full month LME cash average trade is the 2nd business day of the month following the average month. Using the same September 2025 example, the last pricing date in September 2025 is Tuesday the 30th of September. Therefore the prompt date for a September 2025 cash average trade would be Thursday the 2nd of October 2025.

What this means in practice is that each of your CSP trades has its prompt date adjusted from cash, to the second business day of the following month. Inevitably this means that there will be a cost or a gain from executing a cash average trade. If you are selling futures over the average of a month, you will need to borrow those positions from cash to the 2nd business day of the following month. If there is a contango at the time you execute the average trade, you should gain money from borrowing each of the CSP positions. This contango won't necessarily resemble the month over month spread, as you are essentially trading the interday spreads from each CSP as shown in the below table.

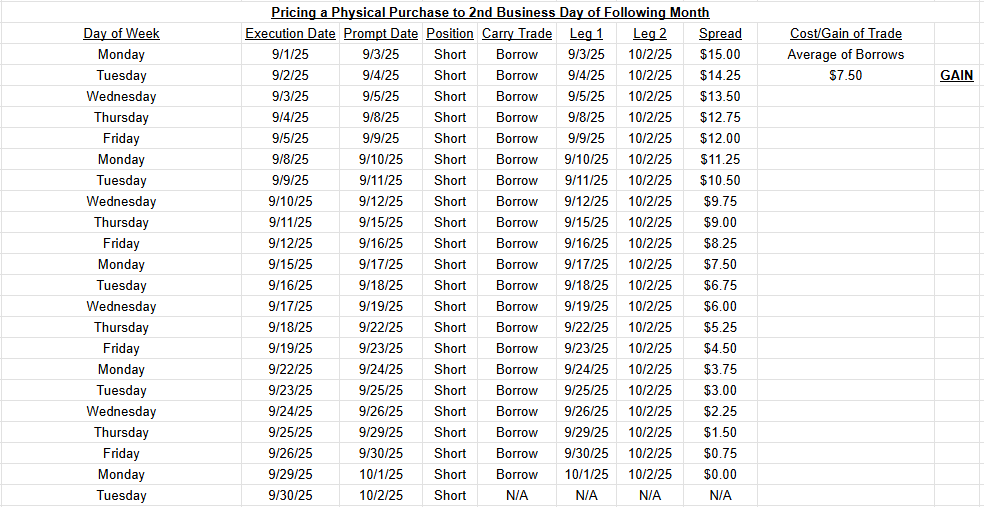

Carries involved in selling the cash average of September prompt the 2nd business day of October

In this example, the market is in a contango each day from the start of September through to the 2nd business day of October. So in this case, selling the cash average, which creates a need to borrow those short positions, results in a gain of $7.50/mt - the average of each days' contango through to the 2nd of October. The cash position from the last business day in September (Tuesday September 30th) does not need its prompt moving since it is already sitting on the 2nd business day of October.

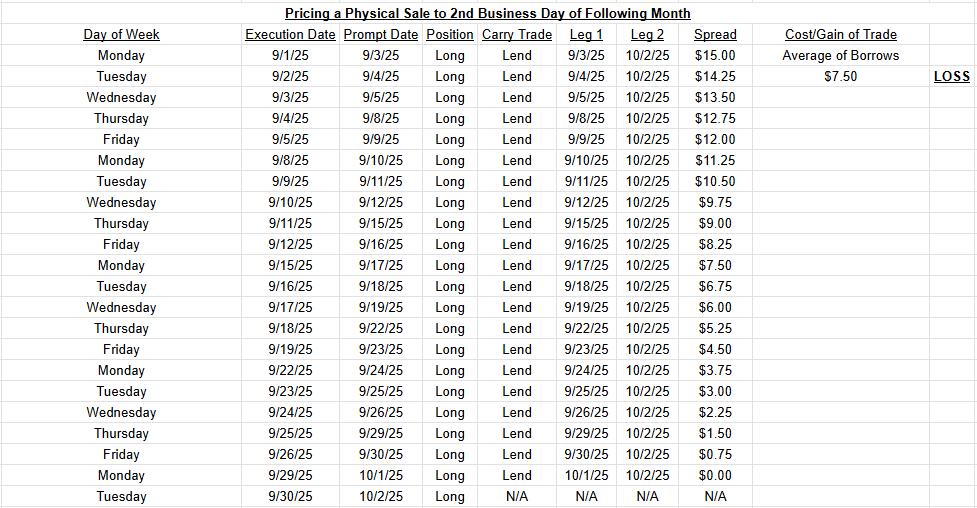

Of course, if this contango still existed but you were pricing a physical sale, and hence were buying futures over the cash average, the carry trades would be lends instead of borrows as shown below.

Carries involved in buying the cash average of September prompt the 2nd business day of October

In this example, because we are long futures on each cash position, in order to adjust them to the second business day of October, we are required to lend those positions. Lending in a contango means selling at a lower price and buying at a higher price, hence why this results in a loss.

In reality, when you execute an averaging trade, you don't see all of these individual carry trades. Your broker will quote you a single price for buying or selling the monthly average. But the price they quote you will be based on all of the interday spreads between prompt dates.

Other Averaging Structures

For those companies that are managing their futures positions on a 3rd Wednesday to 3rd Wednesday basis, they may not want to have a futures position sitting on the 2nd business day of a month. In this case, they can execute an average trade that has the prompt date of the 3rd Wednesday of the average month. For example, executing an trade for the cash average of September, prompt the 3rd Wednesday of September. This is what is known as a month-on-month average, in this case, Sep-on-Sep.

The carries, and therefore the price quoted for this average trade will be different from the price quoted in the above examples.

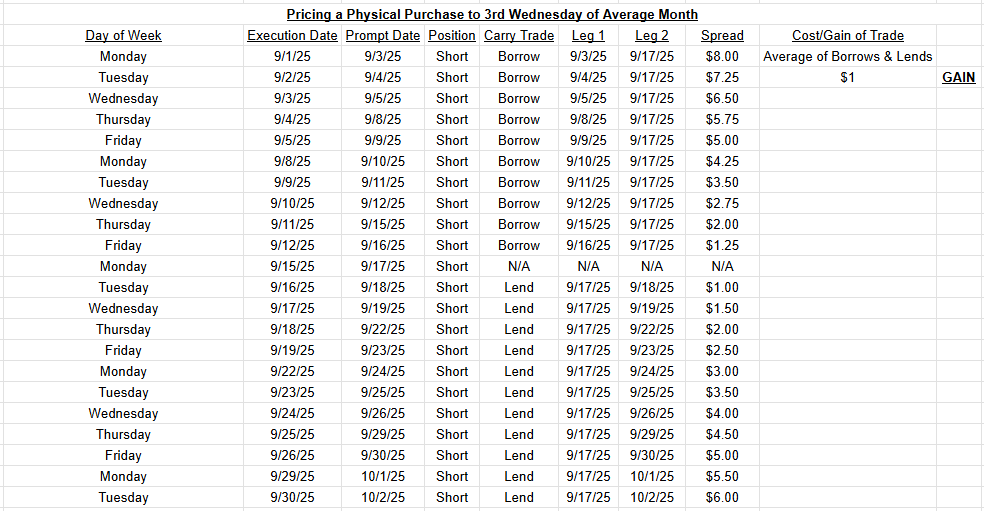

Carries involved in selling the cash September average prompt the 3rd Wednesday of September

For a customer selling the cash average of September prompt 3rd Wednesday of September, they are still short the entire month, and will still be borrowing the first half of the month to the 3rd Wednesday, in this case September 17th. However, for those cash positions that fall after the 3rd Wednesday, they will need to lend them to move the short positions back to the 3rd Wednesday. So while they are gaining from borrowing in a contango in the front half of the month, they are losing by lending in a contango in the back half of the month. In this example, the gain of selling the cash average Sep-on-Sep is only $1/mt.

Here, the CSP that does not require any carry trade is the Monday-prior to the 3rd Wednesday as that cash position is already prompt the 3rd Wednesday.

The opposite carries are required for a customer that is buying the September cash average prompt the 3rd Wednesday of September.

Carries involved in buying the cash September average prompt the 3rd Wednesday of September

Here the customer is long each of the cash prompt dates so they need to lend the front half of the month to the 3rd Wednesday and borrow the second half of the month to establish one long position on the 3rd Wednesday. Because the contango in the front half of the month is slightly larger than the contango in the back half of the month, they are losing more on their lends than they are gaining on their borrows so this average trade comes at a cost of $1/mt.

Of course, there is no requirement to place a month-on-month average trade, or execute the trade prompt the 2nd business day of the following month. Companies that are booking averages may try to line up the prompt dates to future purchase or sales pricing periods (QPs) if they are already known.

Let's say for example that a trader is pricing a physical purchase of the average of September, but they know that the purchase will be allocated to a physical sale that is pricing in November. They can simply request their September cash average trade to be prompt the 3rd Wednesday of November and the broker will price the trade accordingly.

Carry trades involved in selling the September cash average prompt the 3rd Wednesday of November

In this example, each of the short cash positions in September is being borrowed all the way through to the November 3rd Wednesday and the trade is capturing all of those spreads. Using the contangos shown in the example would lead to this average trade resulting in a gain of $17/mt.

The opposite trades would be required if it was a physical sale being priced early and allocated to a physical purchase that wasn't pricing until November.

Carry trades involved in buying the cash average of September prompt the 3rd Wednesday of November

Because this trade involved lending those long positions out of each days' cash through to the 3rd Wednesday of November, and the market is in a contango, the result is a $17/mt loss.

Obviously traders will look to manage their physical QPs between their purchases and sales to try and maximize profits by pricing contracts that result in borrowing in times of contango and lending in times of backwardation.

Combining Positions

Customers needing to execute average trades should also be combining all of their physical purchases and sales contracts to give them one net position, and executing an average trade in one direction only. For example, a trader that is pricing 5,000mt of physical purchases and 3,000mt of physical sales over the same September cash average, would combine those two positions to give a net physical position of buying 2,000mt over the September cash average. They would then execute one average trade to sell 2,000mt over the September cash average, saving themselves paying double commission and a bid/ask spread.

It's not only customers that perform this netting operation. Brokers will also be combining all of their customer requests to give them one position - either a net buyer or net seller over the average. This is why it's always a good idea to finalize your averaging with your broker a day or two in advance of the start of the month, or at least give them a good idea of your position. This gives them the ability to square their positions, and potentially give you a better fill. If nothing else you will be a better customer than one that waits until 30 minutes before the 2nd ring on the first day of the month to send in an average order. This will leave the broker with a last minute position that, depending on the size, may change their approach to the average that month.

It is also this netting that customers the ability to buy or sell as little as 1 lot over a monthly average even when on the face of it, that's not enough tonnage to spread out over 20+ days. Your 1/5/10/etc. lot position is either offsetting, or simply increasing the overall position of that particular broker.

Learn More

By understanding the mechanics behind how prices are constructed, you will be able to add more value to your team. For those looking to turbocharge your LME knowledge, enroll in the London Metal Exchange learning course in partnership with Perfectly Hedged LLC on September 8-12 where we will cover the full spectrum of pricing features available to mitigate risk on the LME. For more information email samuel.basi@perfectlyhedged.com